19 Nov, 2010

Op-Ed Commentary: Chris Devonshire-Ellis

Nov. 19 – Indochina, that area of Southeast Asia that so evocatively describes colonialism, decadence, war and strife, yet encompasses some of the world’s most beautiful archaeological and natural wonders. As a practice, my firm Dezan Shira & Associates established offices in Vietnam nearly three years ago, and we have long been attracted to this part of Asia. From the very subliminal Frenchness that still pervades, to the influence of the Southern Chinese, the region is a potpourri of influences and mystery.

Nov. 19 – Indochina, that area of Southeast Asia that so evocatively describes colonialism, decadence, war and strife, yet encompasses some of the world’s most beautiful archaeological and natural wonders. As a practice, my firm Dezan Shira & Associates established offices in Vietnam nearly three years ago, and we have long been attracted to this part of Asia. From the very subliminal Frenchness that still pervades, to the influence of the Southern Chinese, the region is a potpourri of influences and mystery.

Today, parts of Cambodia, Laos and Vietnam are increasingly being seen as ripe for potential investment. Indochina continues to open up its interior, allowing access across lands previously distant, and lies directly between the wealthy consumer markets of Singapore, Thailand, Malaysia and China. Talk is of opportunity and optimism, yet the three countries have distinctly different demographics and have evolved along rather different lines. While the naive may lump Laos and Cambodia together as “mini Vietnams” or even classify them as quasi vassal states of China, the reality is rather different. In this article we’ll take a look at each of these emerging economies and make comparisons.

As can be seen, the size and population of each of the three countries varies considerably. So too do the geophysical locations, Laos is completely landlocked, and must rely on overland transportation to get goods in and out of the country. Cambodia has a relatively small coastline, with a major deep water port on the west coast at Sihanoukville, about 1,000 kilometers from Singapore. Vietnam enjoys a significant coastline and has several major ports along the east coast of the country, including Ho Chi Minh City. The geophysical position of each of these countries therefore determines a great deal of their success at being able to have developed their international trade. Accordingly, it is no surprise to see Vietnam’s GDP, with its more advanced coastal port facilities, as far higher than that of either Cambodia or Laos.

Indochina is changing; new road and rail routes have been developed and are opening up the interior regions. Ultimately, all these countries will benefit from the Singapore-China rail track, expected to be completed by 2015. This project, ultimately link Beijing with Singapore with stops in between, made serious progress last month with the completion of Cambodia’s refurbished railway, now capable of handling freight trains one kilometer long. Vietnam is starting work on upgrading its 1,700 kilometer line from Hanoi to Ho Chi Minh City, while China is already underway with breaking ground on a spur from Yunnan Province to Laos, and has also agreed on a joint venture with Thailand to upgrade some of its rail tracks. Talks are also underway to provide a route from Bangkok to the Myanmar port of Tavoy on the Indian Ocean. That will also traverse Laos and again provide much momentum to opening up Laos to international trade and import and export.

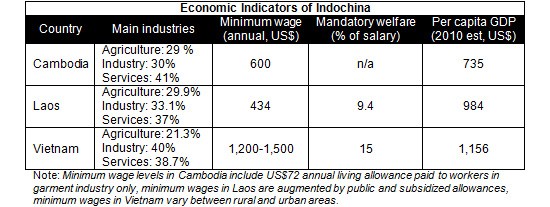

As is apparent, the minimum wage levels represent a significant discount to China, which averages a minimum wage of about US$1,500, but which also has a high mandatory welfare rate of 50 percent. As a rough rule of thumb, this makes Chinese labor at least double the cost of that in Indochina. Not surprisingly, foreign investment is starting to pour into these countries, including from China. What may be surprising to many readers is that it is not China that dominates the region. That honor belongs to Thailand.

China has in the past engaged in invasions and wars in the region, and its presence is still felt to be something of a strategic threat. Accordingly, it is Thailand that holds the balance of trade power within the region (not altogether surprisingly, as it shares borders with both Laos and Cambodia, and does not have the aggressive history in the region that China has). Of note also is the presence of the United States as a major trade partner within the region as well as the European Union, notably led by France as an ex-colonial power, Japan and nearby Singapore.

Intra-ASEAN trade is set to massively increase – all three countries are members of the ASEAN bloc, and intra-ASEAN trade has already expanded significantly with the signing of the ASEAN Free Trade Agreements and the additional signing of the ASEAN FTA with China and India. Clearly, the dynamics of trade within Indochina is going to shift towards ASEAN and Asia in the future. It is this trade, combined with a marked improvement in rail and road infrastructure, that is expected to see GDP growth within Indochina maintain healthy levels.

Some work still needs to be done, especially in terms of developing tax treaties. Tax treaties are important, especially for the attraction of foreign direct investment as they limit the chances to be taxed in two locations for the same profit, and as they can also, dependent upon the agreement, be useful in lowering taxes in areas of international trade such as withholding taxes, taxes on royalties and even dividends. Here is a breakdown of the DTA signed by each of the three Indochina countries:

Cambodia

- Cambodia currently has no double tax treaty agreements in place, but is a member of ASEAN and is expected to implement its ASEAN DTA by 2012

- Bilateral Agreements for the Protection and Promotion of Investment have been signed with China, Germany, Indonesia, Malaysia, Singapore, South Korea, Sweden and Thailand

Laos

- Laos has signed DTA agreements with China, Kuwait, North Korea, South Korea, Thailand and Vietnam and is awaiting ratification for agreements with Brunei, Myanmar and Russia.

Vietnam

- Vietnam has been highly active in pursuing a policy of DTA in order to assist with the attraction of FDI into the country. It has signed DTA agreements with the following countries: Algeria, Austria, Australia, Bangladesh, Belarus, Belgium, Bulgaria, Brazil, Brunei, Canada, China, Cuba, Czech Republic, Denmark, Egypt, Finland, France, Germany, Hungary, Iceland, India, Indonesia, Italy, Japan, North Korea, South Korea, Laos, Luxembourg, Malaysia, Mongolia, Myanmar, Netherlands, Norway, Pakistan, Philippines, Poland, Romania, Russia, Seychelles, Singapore, Spain, Sri Lanka, Sweden, Switzerland, Taiwan, Thailand, Ukraine, United Kingdom, and Uzbekistan.

As can be seen, both Laos and especially Cambodia have some catching up to do with establishing DTAs on an international basis. Both appear to be taking their time to assess the impact of their ASEAN DTA agreements before making such arrangements a cornerstone of their foreign policy. No doubt this will start to kick in over the next couple of years, in which case trade and development in Laos and Cambodia will become more attractive. It is significant that Cambodia has not reached a bilateral agreement with China.

Summary

The regional dynamics of Indochina are more convoluted than they appear. Assumptions that China is making significant inroads into the region appear unfounded; in fact the ethnicity, religious and cultural background of each of the three countries are closer to Thailand than they are to China, and those ties remain strong, and perhaps increasingly so in the face of perceived Chinese aggression, particularly towards Vietnam. Such behavior does not sit well with Vietnam’s neighbors, who fear a strong Chinese presence on their doorstep. This indeed is recognized in the makeup of ASEAN itself, which specifically excludes China from membership.

In fact, Chinese influence in Indochina is typically overstated. Although Chinese ethnicity makes itself felt in terms of the architecture, temples and cuisine, especially in North Vietnam and Hanoi, the fact remains that many ethnic Chinese here are not in fact Chinese nationals but descendants of Chinese traders from several generations who have settled in the area. This is especially true of the millions who fled Yunnan and Guangxi Provinces during the rampages of the Cultural Revolution. Many too, were rich merchants who fled the rise of the Communist party, only to find themselves in a similar uprising in Vietnam. The presence of ethnic Chinese is monitored by each of the respective Indochinese governments, wary of permitting too sizable a Chinese diaspora to dilute their own culture. China is kept at arm’s length here, and nationalism and the ancient Khmer culture still reign supreme over Chinese expansionist claims and theories.

What is increasingly apparent is that, as a bloc, Indochina represents a closely knit group of three ex-colonized nations that tend to stick together with their independence – very much a source of national pride and diplomatic strategy. Hard won independence and wars have made these nations wary of developing a large dependence upon trade with China, despite the proximity and wealth of the country. Indochina, it seems, is not about to be seduced by China anytime soon. ASEAN beckons instead, and it is worth remembering that ASEAN is comprised of 10 member states: Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam. If combined as one nation, it would be the ninth largest in the world with a population of 580 million and a GDP of US$1.5 trillion. That represents the future independence of these nations; safety in numbers, and a significant amount of people, resources and wealth to balance against pressure from the east.

Indochina’s Southeast Asian trade will only increase as regional infrastructure and especially road and rail links further integrate them with one another and permit access to the interior regions. Growth in these markets will continue for the foreseeable future, and some may be viewed as alternatives to China, especially for labor intensive industries, agriculture and garments. Access meanwhile to commodities in the inner regions of Indochina will continue to attract foreign investment, as will the commencement of selling products to a small, yet emerging middle class, especially in Vietnam. Indochina remains an evocative and increasingly dynamic region, quite distinct from its larger neighbor, and remains one that will keep China at bay while developing trade links with the rest of ASEAN and beyond. As an alternative, Indochina, and the countries of Cambodia, Laos and certainly Vietnam appear poised for sustainable and long term growth for some years to come.

Chris Devonshire-Ellis is the principal and founding partner of Dezan Shira & Associates, establishing the firm’s China practice in 1992. The firm now has ten offices in China, five in India, and two in Vietnam. For advice over China strategy, trade, investment, legal and tax matters please contact the firm at info@dezshira.com. The firm’s brochure may be downloaded here.

Chris also contributes to the Asia Briefing publications India Briefing, Vietnam Briefing, and 2point6billion.com.

No comments:

Post a Comment